In 2025, global fraud losses cost businesses and financial institutions hundreds of billions of dollars, eroding customer trust and disrupting operational stability.

Without the right controls and risk management strategies in place, these threats can escalate and undermine long-term growth and security.

In this article, you’ll learn everything you need to know about fraud prevention so you can understand the risks, apply the right safeguards, and protect your institution with confidence.

Key takeaways

- Fraud prevention is proactive, not reactive

Fraud prevention focuses on stopping fraud before losses happen. Financial institutions use identity verification, real-time transaction monitoring, machine learning, and behavioral analytics to catch suspicious activity early and reduce financial and reputational damage.

- Fraud threats are growing in scale and complexity

From identity theft and account takeover to synthetic identity fraud and business email compromise, today’s fraud schemes are more sophisticated than ever.

- Layered strategies work best

Effective fraud prevention combines real-time risk scoring, AI-driven analytics, cross-institution intelligence sharing, and ongoing employee and customer education. Institutions that integrate technology, shared data, and human awareness detect fraud faster and reduce overall exposure.

- There are real tradeoffs to manage

Strong fraud controls reduce losses, improve compliance, and build customer trust. However, institutions must balance implementation costs, evolving fraud tactics, false positives, and data privacy concerns.

- The right partner can dramatically reduce losses

VALID Systems helps banks stop fraud in real time with solutions such as CheckDetect, InstantFUNDS©, INclearing Loss Alerts, and the VALID Fraud Consortium Edge. With documented results and significant reductions in manual review time, VALID delivers measurable protection across every deposit channel.

What is fraud prevention?

Fraud prevention refers to the strategies, technologies, and policies organizations use to detect, deter, and stop fraudulent activity before it results in financial loss, regulatory risk, or reputational damage.

Banks and other financial institutions rely on a combination of identity verification, real-time transaction monitoring, machine learning, and behavioral analytics to identify suspicious activity early.

By continuously analyzing customer behavior and transaction patterns, these systems help protect both the institution and its customers from evolving financial threats.

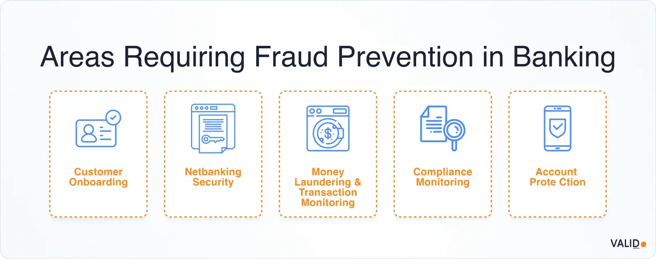

Different types of fraud you should know about

Recognizing the most common types of fraud makes it easier to spot warning signs early and put the right safeguards in place.

Identity theft

Criminals steal personal information, such as Social Security numbers or credit card details, to impersonate victims. Using this data, they may open new accounts or take control of existing ones, leading to financial losses and long-term reputational damage.

In 2024, the US Federal Trade Commission received more than 1.13 million identity-theft complaints, with total losses exceeding $12.7 billion.

Account takeover (ATO)

Fraudsters gain unauthorized access to legitimate customer accounts and take control of them. If successful, they may change login credentials or payment information, then steal funds or make unauthorized purchases. Account takeover is one of the fastest-growing forms of fraud, with US institutions reporting $15.6 billion in losses in 2024.

Check and deposit fraud

Despite the growth of electronic payments, check fraud remains a significant problem. Criminals exploit weaknesses in the check deposit process by using forged or altered checks or creating counterfeit payees.

Card fraud

Card fraud involves the unauthorized use of debit or credit cards, whether in person or online through card-not-present transactions. This type of fraud continues to rise worldwide. In 2023, US payment cards accounted for $14.32 billion in fraud losses, driven largely by online transactions.

ACH and wire fraud

These schemes involve unauthorized electronic fund transfers. One of the most damaging forms is Business Email Compromise (BEC), in which fraudsters spoof or gain access to legitimate email accounts to redirect payments to fraudulent destinations.

Synthetic identity fraud

Criminals create fake identities by blending real and fabricated information to open fraudulent accounts or secure loans. Because parts of the identity appear legitimate, this type of fraud is especially difficult to detect.

Best strategies for effective fraud prevention

Effective fraud prevention requires a proactive, layered approach that combines real-time technology, shared intelligence, and human awareness.

Here are practical, proven strategies that help financial institutions spot fraud sooner, act quickly, and reduce losses across all deposit channels:

1. Implement real-time risk scoring

Real-time risk scoring strengthens frontline defenses by assigning a fraud probability score to every deposit-related action, whether it occurs through a teller, ATM, or digital channel. This allows banks to intervene immediately.

How to do it:

- Deploy AI-driven models that evaluate transaction amount, account age, historical behavior, velocity patterns, and channel data to generate a real-time fraud risk score.

- Establish clear, tiered risk thresholds aligned with your institution’s fraud tolerance and operational capacity.

- Automatically place holds, generate alerts, or escalate high-risk deposits for immediate investigation.

- Route medium-risk transactions to back-office review teams with defined service-level agreements (e.g., review within 15 minutes).

- Integrate deposit channel metadata, such as IP address, device fingerprint, geolocation, or ATM ID, with historical transaction behavior to improve anomaly detection accuracy.

Worth knowing:

Solutions like VALID Systems’ CheckDetect extend real-time risk scoring to teller lines and ATMs, analyzing deposits before posting and triggering immediate alerts.

By identifying more than 75% of loss-bound check items prior to posting, institutions can act decisively, placing holds or escalating reviews while the transaction is still in motion.

2. Use data-driven analytics

Modern fraud schemes evolve quickly, making static rules and manual reviews increasingly ineffective.

Data-driven analytics powered by AI and machine learning enable banks to identify suspicious activity as it happens by recognizing subtle behavioral changes and emerging patterns that traditional controls often miss.

How to do it:

- Deploy machine learning models that analyze transaction and account activity in real time to identify unusual or high-risk behavior.

- Incorporate behavioral analytics, including device fingerprints, geolocation signals, session behavior, and transaction velocity, to establish a dynamic customer baseline.

- Flag deviations from normal customer behavior for automated action or analyst review based on risk severity.

- Continuously retrain models using confirmed fraud outcomes to improve accuracy and reduce false positives over time.

- Combine AI-driven insights with existing rules and human review workflows to ensure explainability and regulatory alignment.

3. Leverage cross-institution fraud intelligence

Fraud rarely targets a single bank. Criminals reuse accounts, devices, and methods across multiple institutions, often moving faster than one organization can detect on its own.

Consortium-based fraud intelligence addresses this gap by enabling banks to share high-risk indicators and patterns, thereby strengthening defenses across the entire ecosystem.

How to do it:

- Join a reputable national or regional fraud intelligence consortium that aligns with your regulatory and privacy requirements.

- Ingest anonymized alerts and risk indicators, such as suspect accounts, compromised check series, mule networks, or origin banks, directly into your fraud detection systems.

- Enable real-time matching so deposits, logins, or transactions are screened against consortium-provided risk signals as they occur.

- Automatically flag or escalate activity that matches blacklisted or high-risk behaviors identified by other consortium members.

- Apply elevated risk scores to transactions linked to previously closed, compromised, or fraud-associated accounts across the network.

Worth knowing:

Edge Data Consortium connects your institution to a powerful, cross-bank intelligence network.

By analyzing behavior patterns across multiple institutions, Edge uncovers sophisticated fraud schemes, especially first-party and synthetic fraud, that are difficult to spot in isolation.

Here is what it does:

- Detects fraud patterns that extend beyond your own institution

- Monitors risk across account openings, check activity, loans, and more

- Delivers actionable insights that support GLBA compliance

4. Focus on employee and customer education

Even the most advanced detection systems can be undermined if employees or customers are unaware of common scam tactics or fail to follow established security protocols.

Consistent education builds a strong first line of defense by empowering people to recognize and respond to fraud risks before losses occur.

How to do it:

- Provide regular, role-specific fraud training for employees, with added emphasis on frontline staff who interact directly with customers and transactions.

- Train staff to recognize common red flags, such as phishing emails, social engineering attempts, unusual urgency, or requests that fall outside normal processes.

- Reinforce clear escalation and reporting procedures, so employees know exactly how and when to raise concerns.

- Conduct periodic simulations or tabletop exercises to test employee readiness and reinforce proper responses.

- Educate customers through clear, ongoing communications about prevalent scam tactics and protection methods.

Benefits and challenges of fraud prevention

Fraud prevention offers significant advantages for financial institutions, but it also poses potential drawbacks that must be carefully managed. Below are the key benefits and challenges you should be aware of:

Benefits:

- Reduced financial losses: A robust fraud prevention system helps detect and stop fraudulent activities. By identifying suspicious behavior early, organizations can minimize direct financial losses, protect revenue streams, and safeguard assets.

- Stronger customer trust: Customers are more likely to remain loyal to organizations that actively protect their data and transactions. Demonstrating a strong commitment to fraud prevention enhances credibility, strengthens relationships, and reinforces the organization’s reputation.

- Regulatory compliance: By maintaining proper controls, monitoring systems, and reporting procedures, organizations reduce the risk of penalties, lawsuits, and regulatory sanctions.

- Operational efficiency: Preventing fraud reduces the time and resources spent investigating incidents, resolving disputes, and recovering funds. Streamlined detection systems and clear internal processes allow staff to focus on productive activities rather than crisis management.

- Data-driven decision making: Modern fraud prevention tools rely on analytics and monitoring systems that provide valuable insights into customer behavior and transaction patterns. These insights can improve risk assessment, strengthen internal controls, and support smarter strategic decisions.

Challenges:

- High implementation costs: Establishing effective fraud prevention systems often requires significant investment in technology, software, skilled personnel, and ongoing training. For many organizations, especially smaller ones, these costs can be substantial.

- Evolving fraud tactics: Organizations must continuously update systems, refine detection models, and stay informed about emerging threats, making fraud prevention an ongoing effort rather than a one-time solution.

- False positives and customer friction: Overly strict fraud controls can mistakenly flag legitimate transactions. This may lead to customer inconvenience, delayed services, and frustration, potentially harming customer experience and loyalty.

- Data privacy concerns: Fraud prevention relies heavily on collecting and analyzing customer data. Balancing effective monitoring with respect for privacy laws and ethical standards can be complex and sensitive.

- Internal resistance and cultural barriers: Implementing stricter controls may lead to resistance from employees who see them as burdensome or intrusive. Building a culture of compliance and awareness requires consistent communication, training, and leadership support.

Fraud prevention vs. fraud detection: Key differences

Although fraud prevention and fraud detection are closely related, they play distinct roles in managing fraud risk. Understanding how they differ and how they work together helps financial institutions minimize losses and protect customers.

Here are the key differences between fraud prevention and detection:

|

Fraud prevention |

Fraud detection |

|

|

When it happens |

Takes place before a fraud attempt occurs |

Takes place during or immediately after a fraud attempt |

|

Main objective |

Reducing the likelihood of fraud occurring in the future |

Identifying fraudulent activity and limiting potential impact |

|

Approach |

Proactive measures designed to stop fraud before it starts |

Reactive and real-time monitoring of suspicious activity |

|

How it works |

Applies policies, rules, and safeguards that make fraud more difficult to carry out |

Continuously analyzes activity to detect and flag suspicious behavior |

|

Customer impact |

Helps protect customers with minimal disruption when thoughtfully implemented |

Reduces false positives, leading to a smoother customer experience |

|

Operational benefit |

Lowers overall fraud exposure and long-term risk |

Improves fraud team efficiency and speeds up response times |

Fraud prevention and fraud detection are complementary strategies. Prevention makes it harder for criminals to succeed, while detection identifies and mitigates threats that slip through defenses.

A strong fraud strategy combines proactive safeguards to reduce risk with intelligent detection systems to quickly respond when suspicious activity occurs.

This is exactly where VALID can help you!

Strengthen fraud prevention with VALID Systems

With more than 20 years of experience in risk-based decisioning and deep fraud-detection expertise, VALID helps financial institutions identify and prevent losses before they occur.

Trusted by leading institutions such as PNC Bank, TD Bank, and Truist, VALID processes over $4 trillion in annual check volume, while delivering fraud prevention capabilities that extend well beyond checks alone.

How VALID can help you:

- CheckDetect: Instantly identifies suspicious activity across mobile, ATM, and in-branch transactions, enabling banks to stop fraud in real time rather than reacting after losses occur.

- InstantFUNDS©: Delivers sub-second decisioning for check deposits, balancing fraud risk and customer experience by providing guaranteed funds availability when appropriate.

- INclearing Loss Alerts: Leverages AI and behavioral analytics to detect abnormal patterns during transaction processing, uncovering threats that traditional systems often fail to identify.

- VALID Fraud Consortium Edge: A collaborative intelligence network powered by partnerships with leading US banks, providing access to broader fraud insights and emerging threat patterns while maintaining strict data privacy standards.

With these capabilities, VALID delivers results that go beyond theory:

- 74% year-over-year fraud loss reduction at PNC

- Fraud loss rates reduced from 22 bps to 2 bps at FNB

- 75% reduction in manual fraud review time at Commerce Bank

Contact us today to learn how you can reduce fraud losses, accelerate decisioning, and strengthen protection across every deposit channel.