Did you know that by 2028, global losses to online payment fraud are projected to reach $362 billion?

For financial institutions, this growing risk makes effective oversight of transaction activity more important than ever.

Transaction monitoring helps banks and other institutions detect early warning signs, such as unusual spending patterns or unexpected account behavior, and trigger alerts before potential fraud or financial crime escalates.

In this article, we’ll explore everything you need to know about transaction monitoring alerts so you can understand how they work, why they matter, and how they support stronger compliance and risk management.

Key takeaways

- Transaction monitoring alerts are the first line of defense against financial crime

Banks use automated alerts to detect unusual or suspicious activity in real time, helping identify fraud, money laundering, and other illicit behavior before losses occur.

- Regulatory compliance depends on effective alerting and follow-up

Laws require institutions to monitor and report suspicious activity. Weak alert systems or poor escalation can lead to massive fines, regulatory sanctions, and long-term oversight.

- Alerts protect both customers and a bank’s reputation

Beyond financial losses, failures in monitoring and internal controls can erode customer trust and brand credibility, as seen in major banking scandals that led to leadership fallout and years of reputational damage.

- Not all alerts are equal, and false positives are a major problem

Traditional rule-based systems generate huge volumes of low-quality alerts, overwhelming compliance teams and increasing the risk of actually dangerous activity being missed.

- Modern, intelligence-driven platforms are the way forward

As fraud tactics and transaction volumes grow, banks need real-time, AI-driven monitoring that adapts to behavior, reduces unnecessary alerts, and surfaces true risk faster. Solutions like VALID are designed to meet this need by reducing false positives, improving detection accuracy, and protecting institutions without adding friction for customers.

What are transaction monitoring alerts?

Transaction monitoring alerts are automatic notifications generated by a bank’s monitoring systems when unusual or suspicious transactions are detected.

Modern financial institutions continuously track customer account activity for anomalies. If a transaction (or series of transactions) matches certain risk criteria or “red flag” patterns, the system will send an alert to compliance officers for review.

Why are transaction monitoring alerts important?

Transaction monitoring alerts are essential for regulatory compliance and effective risk management, acting as a bank’s first line of defense against financial crime. Here is why they are important for financial institutions:

1. Preventing financial crime

Alerts help banks identify money laundering, fraud, and other illegal activity early. By flagging suspicious behavior in real time, banks can act quickly and stop criminals before damage is done.

With the rapid growth of digital payments, effective monitoring is more important than ever, as the sheer volume of daily transactions would otherwise enable financial crime to evolve unchecked.

2. Regulatory compliance

Banks and credit unions are legally required to monitor transactions and report suspicious activity. When institutions fail to act on these warnings, the consequences can be severe.

For example, in 2021, FinCEN fined Capital One $390 million after the bank admitted it had failed to file thousands of Suspicious Activity Reports (SARs).

Strong alert systems are important not only for detecting risk but also for preventing regulatory violations and costly fines.

3. Protecting the institution and its customers

A well-tuned alert system can prevent direct losses and protect customers from theft. It also shields the bank’s reputation, demonstrating to customers and the public that the institution can be trusted to detect and prevent illicit activity.

To put it in perspective, consider the Wells Fargo fake accounts scandal. Between roughly 2011 and 2016, employees at Wells Fargo secretly opened millions of unauthorized customer accounts (checking, savings, and credit cards) to meet aggressive sales targets.

This case is recognized as a reputational collapse, leading to the following:

- Massive loss of customer trust: After the misconduct became public, many customers closed their accounts or moved to other banks.

- Public outrage and media backlash: The scandal dominated headlines globally and became synonymous with unethical banking practices.

- Regulatory punishment and lasting stigma: Wells Fargo paid over $3 billion in fines and settlements. Additionally, the US Federal Reserve imposed a growth cap on the bank, a rare and severe penalty that reflected a lack of trust in its governance and controls.

- Leadership fallout: The CEO resigned, senior executives were fired or banned from the industry, and the bank spent years rebuilding its image.

The scandal persisted for years because internal controls, alerts, and oversight failed. For example:

- Customer complaints were ignored or minimized.

- Internal warnings were not escalated properly.

- Risk and compliance systems failed to stop the behavior early.

4. Supporting law enforcement

Suspicious transaction alerts don’t just stop at internal reviews. They feed directly into the formal reports that law enforcement depends on.

In the US alone, banks filed 4.7 million suspicious activity reports (SARs) in 2024, averaging 12,870 filings every day.

These reports play a meaningful role in real investigations. For example, more than 87% of recent IRS criminal cases recommended for prosecution were supported by a Bank Secrecy Act (BSA) report, such as a SAR.

Different types of transaction monitoring alerts

There is no single definition of a “suspicious transaction.” As a result, banks configure a wide range of alerts to address different risk scenarios.

Most transaction monitoring systems rely on multiple rules and algorithms to identify unusual or concerning patterns. The sections below describe some of the most common types of transaction monitoring alerts.

1. Large transaction threshold alerts

These alerts flag unusually large transactions or cash movements above certain amounts. Financial institutions set thresholds (absolute values or relative to an account’s normal activity) that trigger an alert when exceeded.

For example, if an everyday checking account that usually sees $1,000 transactions suddenly wires out $50,000, an alert will pop up for review. Such alerts ensure big transfers, which could indicate money laundering or high-value fraud, never go unchecked.

Note: Banks also file Currency Transaction Reports for cash transactions over $10,000 by law, but separate internal alerts may still highlight large electronic transfers or patterns of just under $10,000.

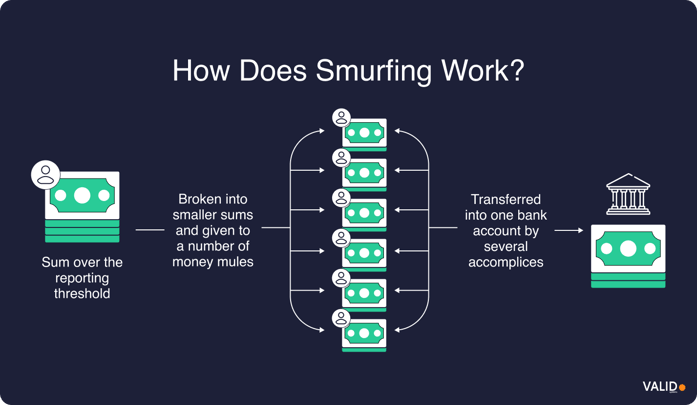

2. Structuring/smurfing alerts

Structuring, or “smurfing”, refers to breaking down a large amount of money into many smaller transactions to avoid detection.

Monitoring systems look for patterns such as multiple transactions just below regulatory limits, repeated cash deposits or withdrawals at different branches on the same day, or other behavior consistent with smurfing.

For instance, if a customer deposits $9,800 in cash several days in a row (just under the $10k reporting threshold), it will trigger a structuring alert.

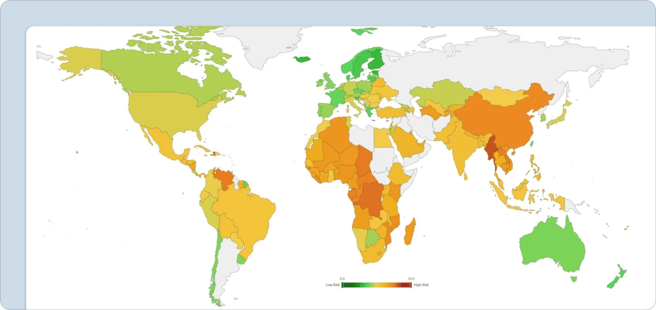

3. High-risk geography or sanctions alerts

Transactions involving certain locations or entities can automatically raise red flags. Banks set up monitoring systems to flag transfers to or from high-risk jurisdictions, such as countries with weak anti-money laundering (AML) controls or a history of terrorism financing.

Below, you can see a global map of money laundering risks in 2024 based on the Basel AML Index.

Similarly, any transaction involving an individual or organization on a watchlist or sanctions list, such as one designated by OFAC, will typically trigger an immediate alert or even a temporary freeze.

For example, a wire transfer to a bank in a country on the FATF high-risk list, or funds sent to an offshore account in a known secrecy haven, would be flagged for closer review.

4. Unusual transaction pattern alerts

Not all alerts are triggered by a single transaction. Many are based on patterns of activity over time. When an account behaves in a way that significantly deviates from its normal usage, it can raise a red flag.

Common examples include:

- Sudden spikes in transaction volume

- A burst of transfers in an account that is usually quiet

- Rapid “in-and-out” movement of funds, where money is deposited and quickly withdrawn

- Unexpected changes in payment behavior, such as an account that typically receives one paycheck per month suddenly getting dozens of payments in a single week

These pattern-based alerts are especially useful for identifying more subtle or intentional activity, such as layering in money laundering schemes.

5. Customer profile deviation alerts

Banks maintain a profile for each customer based on factors such as their occupation, account history, and typical transaction behavior. When activity doesn’t align with what’s expected for that customer, it may trigger an alert.

Situations that commonly raise concerns include:

- Transactions that don’t match the customer’s background, such as a student account receiving large international wire transfers

- Activity outside the customer’s normal scope, like a small, locally focused business sending funds to overseas accounts unrelated to its operations

- Sudden changes in financial behavior that can’t be explained by the customer’s past activity

These alerts are designed to answer a simple question: “Does this transaction make sense for this customer?” If the activity appears inconsistent with the customer’s usual behavior or profile, it warrants further review.

6. Fraud-related alerts

While many transaction monitoring alerts focus on anti-money laundering (AML) compliance, the same systems are also used to detect fraud.

These alerts are designed to identify activity that suggests someone may be attempting to defraud the customer or the bank.

Common fraud-related triggers include:

- A sudden burst of out-of-state or international card purchases, which may indicate a stolen credit card

- Rapid transfers immediately after a login from a new or unfamiliar device, suggesting a possible account takeover

- Purchasing or transfer behavior that doesn’t match the customer’s usual habits

- Signs of identity theft or account compromise, such as unusual locations, devices, or spending patterns

Challenges of transaction monitoring alerts

While transaction monitoring alerts are a critical tool for detecting financial crime, they also come with significant operational challenges. Some of the most common issues financial institutions face include:

- Excessive false positives: Most transaction monitoring alerts are false alarms. This creates heavy pressure on compliance teams, leading to inefficiency, analyst burnout, and the risk that truly suspicious activity may be overlooked.

- High transaction volume and velocity: Rapid growth in transaction volumes, combined with faster payment speeds, makes real-time analysis increasingly difficult. As a result, alerts may be reviewed after the activity has already occurred, delaying investigations and response.

- Data quality issues and system silos: Inconsistent or incomplete customer data across multiple internal systems prevents institutions from building a unified view of customer behavior. Poor data quality reduces detection accuracy and increases the likelihood of both missed risks and unnecessary alerts.

- Inflexible rule-based systems: Many transaction monitoring systems rely on static thresholds that are not regularly reviewed or tuned. These rigid rules struggle to detect more complex or emerging money laundering techniques that fall outside predefined patterns.

- Regulatory pressure and complexity: Financial institutions must comply with various, sometimes inconsistent, regulatory requirements across jurisdictions. Keeping monitoring systems aligned with evolving regulations requires constant updates and increases the risk of compliance gaps.

- Operational bottlenecks and alert backlogs: High alert volumes often lead to investigation backlogs that strain compliance operations. In some cases, alerts can remain open for months, slowing risk mitigation and increasing regulatory exposure.

As transaction volumes increase and fraud tactics evolve, it’s clear that traditional, rule-based monitoring systems alone are no longer sufficient.

Static thresholds, siloed data, and alert-heavy workflows create operational strain while still allowing sophisticated fraud to slip through.

What financial institutions need is real-time, intelligence-driven monitoring systems that can adapt to changing behavior, reduce unnecessary alerts, and surface genuinely high-risk activity faster.

This is where advanced platforms like VALID Systems stand out.

How VALID addresses the biggest transaction monitoring challenges

VALID is an AI-driven risk management and fraud prevention platform that helps financial institutions detect and prevent fraud in real time across digital and check-based transactions.

Its fraud prevention and decisioning platform is designed specifically to overcome the pain points that compliance and fraud teams face every day:

- Fewer false positives, better signal quality: Rather than relying solely on rigid rules, VALID uses machine learning and behavioral analytics to score transactions in real time. This allows institutions to focus on the alerts that truly matter, dramatically reducing noise, alert fatigue, and investigation backlogs.

- Real-time decisioning, not delayed reviews: VALID evaluates risk at the moment of transaction or deposit, not hours or days later. This enables faster intervention, earlier fraud prevention, and stronger protection for both the institution and its customers.

- Behavioral and network-based intelligence: By analyzing payer behavior, depositor patterns, and relationships between accounts, VALID detects fraud that traditional transaction monitoring systems often miss, especially subtle schemes such as check kiting, RDC fraud, and coordinated account abuse.

- Built for scale and operational efficiency: With fewer than 0.5% of items generating alerts and up to 74% reduction in manual review time, VALID helps teams operate efficiently even as transaction volumes grow.

- Risk reduction without customer friction: VALID’s solutions remove unnecessary holds and delays, enabling banks to prevent fraud while delivering fast, seamless customer experiences.

- Guaranteed protection against returned checks: VALID guarantees all customer-selected checks against returns, eliminating refund exposure from check fraud.

- Shared intelligence through Edge: VALID’s Edge Data Consortium connects participating institutions via secure, AI-powered shared intelligence, enabling earlier fraud pattern identification and stopping repeat offenders before losses spread across banks.

Contact us today and see how VALID transforms transaction monitoring into a faster, smarter, and more effective defense against fraud and financial crime.

FAQ:

1. What is transaction monitoring?

Transaction monitoring is the process banks use to review customer account activity.

It involves analyzing current and past transactions, along with customer information and interactions, to build a complete picture of how an account is being used and to spot unusual or potentially risky activity.

2. What’s the difference between a SAR and a CTR?

The key difference is suspicion versus threshold.

- SARs are filed when a bank suspects criminal or unusual activity, regardless of the dollar amount (as long as it meets reporting requirements).

- CTRs (Currency Transaction Reports) are required for cash transactions over a set threshold, even if there is no suspicion of wrongdoing.

3. What are red flags in transaction monitoring?

Red flags are warning signs that may indicate potential financial crime or misuse of an account. Common examples include:

- Transactions that don’t match a customer’s normal behavior or profile

- Large or frequent transfers with no clear explanation

- Sudden changes in account activity patterns

4. What triggers a bank to file a SAR?

A bank must file a Suspicious Activity Report (SAR) when it detects activity that may involve criminal activity.

This could include obvious signs of wrongdoing, such as a customer admitting to a crime or attempting to offer a bribe. A SAR must be filed if the suspicious activity involves or totals $5,000 or more in funds or assets.