Is your institution losing money to unexpected defaults and rising credit losses despite steady lending activity?

According to recent global banking forecasts, credit losses are expected to increase by around 8% in 2026, putting even well-established portfolios under pressure.

When losses rise this fast, the issue isn't just the market. Your credit risk management processes may not be evolving quickly enough to keep pace with changing borrower behavior and economic volatility.

In this article, you’ll learn seven credit risk management strategies that will help you reduce losses, improve credit decisions, and build a more resilient portfolio.

Key takeaways

- Credit risk management is a continuous process, not a one-time decision

Strong credit risk management starts at underwriting but does not stop at loan approval. Ongoing monitoring, pricing, stress testing, and governance are what ultimately protect portfolio quality and limit losses over the life of a loan.

- Looking forward matters more than looking backward

Forward-looking stress testing, predictive analytics, and early warning indicators help institutions anticipate downturns, meet regulatory expectations, and adjust risk before losses materialize.

- Diversification and risk-based pricing are essential shock absorbers

Concentration risk can quickly magnify losses when a single sector or region weakens. Diversifying exposures and aligning pricing and limits to borrower risk helps banks maintain healthier, more resilient portfolios.

- Early detection and intervention reduce losses more than recovery efforts

Continuous monitoring allows lenders to spot borrower stress, behavioral changes, or covenant breaches early. Acting quickly through restructuring, repricing, or tighter controls often prevents small issues from turning into defaults.

- Modern credit risk management must include fraud and transaction-level risk controls

Credit losses are increasingly driven by fraud and operational breakdowns, not just borrower default. VALID helps financial institutions detect risk earlier by combining real-time machine learning, behavioral analytics, and network intelligence.

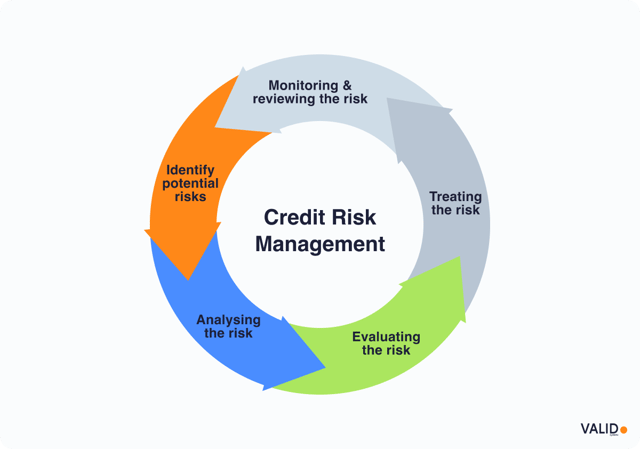

What is credit risk management?

Credit risk management (CRM) is the process of evaluating, monitoring, and reducing the risk that borrowers will default on their loans.

It begins during the loan application stage with a detailed review of the borrower’s financial profile, including income, assets, liabilities, and credit history. The process continues through loan approval, pricing decisions, and ongoing monitoring over the life of the loan.

The main objective of credit risk management is to limit potential losses and maintain a strong, balanced loan portfolio.

Types of credit risks to manage

Credit risk can take many different forms, and each one requires its own approach to managing and reducing potential losses. Below are some of the most common types of credit risk:

- Default risk: Default risk refers to the possibility that a borrower will miss scheduled payments or stop paying altogether. Because no loan is completely risk-free, lenders must carefully evaluate both the borrower’s financial ability and their willingness to repay before extending credit.

- Concentration risk: Concentration risk occurs when a lender has too much exposure to a single borrower, industry, or geographic area. For example, a community bank with half its commercial loan portfolio tied to one industry or city would face significant losses if that market experienced a downturn or collapse.

- Country/Sovereign risk: Country or sovereign risk arises when lending to borrowers located in countries with unstable governments or weak economies. Events such as currency devaluations, trade restrictions, political unrest, or government defaults can prevent borrowers from meeting their obligations.

- Collateral/Recovery risk: This risk involves the possibility that pledged collateral, such as real estate, machinery, or inventory, loses value or cannot be easily sold if the borrower defaults.

- Counterparty risk: Counterparty risk is the chance that a third party, such as a guarantor or insurer, fails to meet its obligations. If a guarantor goes bankrupt or an insurer cannot pay, the lender loses an important backup protection for the loan.

- Interest-rate risk: Changes in interest rates can affect the value of loans and bonds, especially those with fixed rates. When interest rates rise, the market value of existing fixed-rate assets typically falls.

- Operational risk: Operational risk stems from weaknesses in systems, controls, or identity verification processes. Errors or failures can lead to loans being issued to unqualified borrowers, increasing the likelihood of future defaults. Although often categorized separately, these risks ultimately contribute to higher credit losses if they are not detected early.

7 Credit risk management strategies to protect financial institutions

The following strategies offer practical ways for banks to make better credit decisions, protect portfolio performance, and identify risks earlier.

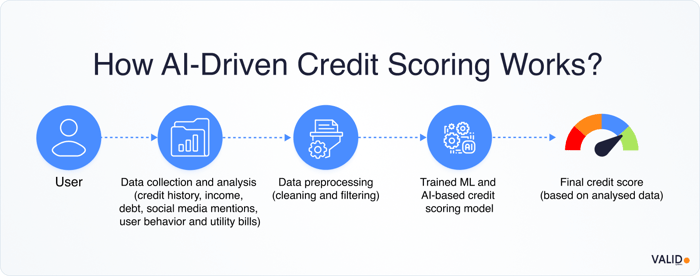

1. Harness data analytics and AI for smarter credit decisions

Traditional credit models rely on a limited set of variables and often miss early or subtle risk signals. Modern lenders are addressing this gap by using advanced data analytics and machine learning to evaluate borrowers more holistically.

By analyzing large volumes of borrower information alongside broader economic indicators, AI-driven models can significantly improve the accuracy of credit scoring and risk assessment.

How to do it:

- Aggregate diverse data sources, including loan performance history, transaction behavior, and alternative data such as utility or rent payments.

- Apply machine learning models to identify complex patterns and correlations that traditional scorecards cannot detect.

- Use predictive analytics to flag early warning signals such as payment irregularities or cash flow stress.

- Continuously retrain models using new borrower and macroeconomic data to keep risk assessments up to date.

- Equip credit analysts with AI-powered tools that surface risk insights and recommendations, rather than relying solely on static scores.

Worth knowing:

While many tools promise AI-driven risk insights, not all are designed to turn complex data into real-time, scalable credit and fraud decisions. VALID operationalizes advanced analytics by combining behavioral, transactional, and network-level data to surface early risk signals that static models often miss.

Here is what VALID does:

- Aggregates behavioral, transactional, and alternative data into a unified decisioning layer

- Applies machine learning to detect complex patterns and early risk signals that traditional models miss

- Scores transactions and accounts in real time to support faster, more accurate decisions

- Continuously learns from new data to adapt to evolving risk and fraud behaviors

- Equips analysts with clear, actionable insights rather than opaque model outputs

Contact us today to learn how AI-driven, real-time decisioning can help you detect risk earlier.

2. Implement forward-looking stress testing

Regulators expect banks to assess how their portfolios would perform under future adverse conditions, not just past cycles. More specifically:

- Frameworks like CECL require banks to incorporate reasonable and supportable forecasts into loss estimates.

- Regulatory programs such as CCAR and DFAST emphasize stress testing at both the portfolio and individual loan level.

Forward-looking stress testing allows lenders to model potential downturns, such as economic recessions, rising interest rates, or sector-specific disruptions, and estimate how those scenarios would impact credit losses.

How to do it:

- Design a range of macroeconomic and idiosyncratic stress scenarios, including severe recessions, rapid rate increases, and concentrated industry shocks.

- Model the impact of each scenario on borrower performance, default rates, and loss severity across portfolios.

- Incorporate stress-test outputs into CECL reserve calculations and capital planning processes.

- Use results to proactively adjust underwriting standards, pricing, or exposure limits before conditions deteriorate.

- Establish governance and review processes to ensure assumptions, models, and outcomes align with regulatory expectations.

3. Diversify the loan portfolio

Concentrated exposure to a single borrower, industry, or region can magnify losses when conditions deteriorate.

Spreading credit exposure across multiple industries and geographies lowers the likelihood that a single shock, such as a real estate correction or technology slowdown, will significantly impair portfolio performance.

How to do it:

- Set internal concentration limits, such as capping exposure to a single industry, geography, or borrower segment at a defined percentage of total loans.

- Regularly review portfolio composition to identify emerging imbalances or sector buildups.

- Use portfolio monitoring tools, such as heat maps and concentration reports, to visualize risk exposures across segments.

- Rebalance originations and adjust growth strategies if concentrations begin to exceed risk tolerance thresholds.

- Incorporate diversification targets into strategic planning and risk appetite frameworks.

4. Strengthen underwriting with collateral and covenants

Strong underwriting goes beyond evaluating credit scores by ensuring the financial institution has meaningful protection if a borrower fails to repay.

By requiring solid collateral and clear, enforceable loan terms, banks can recover losses and spot warning signs early.

How to do it:

- Request the appropriate collateral (such as property, equipment, or unpaid invoices) based on the loan type and the borrower’s risk.

- Be conservative about loan size so the collateral still covers the loan even if markets decline.

- Use personal guarantees or co-signers for riskier loans, especially with small businesses.

- Set clear financial guardrails, like minimum cash flow or liquidity levels, to spot problems early.

- Take action quickly if those guardrails are crossed by talking with the borrower, adjusting loan terms, or restructuring the loan before it defaults.

5. Enable continuous monitoring and early intervention

Credit risk management doesn’t end when a loan is approved. It requires active oversight throughout the entire life of the loan.

Ongoing monitoring helps lenders spot early signs of borrower stress and take action before issues become more serious. In many cases, timely intervention can be the difference between a short-term challenge and a permanent credit loss.

How to do it:

- Use automated monitoring tools to track payments, covenant compliance, updated financial statements, and changes in borrower behavior.

- Incorporate external risk signals, such as news alerts, regulatory actions, or industry trends, into borrower assessments.

- Set up real-time alerts to notify relationship managers of missed payments, declining revenues, or other early warning signs.

- Define clear escalation and review procedures for responding once an alert is triggered.

- Act early when issues arise by restructuring loans, adjusting payment terms, or requesting additional collateral.

6. Apply risk-based pricing and dynamic exposure limits

Not all borrowers present the same level of risk, and loan pricing should reflect those differences.

By aligning interest rates, fees, and exposure limits with a borrower’s risk profile, banks can ensure that returns appropriately compensate for potential losses while also protecting the portfolio from excessive concentrations.

How to do it:

- Tie loan pricing models directly to internal risk ratings or credit scores so higher-risk borrowers are automatically charged higher rates or fees.

- Factor in the probability of default and expected loss severity when setting prices to maintain strong risk-adjusted returns.

- Establish exposure limits at both the borrower and portfolio levels to avoid excessive concentration in one client, industry, or segment.

- Review and recalibrate pricing and exposure limits regularly based on portfolio performance and macroeconomic trends.

- Act proactively by tightening pricing or reducing limits when risk indicators worsen or economic conditions weaken.

7. Maintain strong governance and a risk-aware culture

Strong governance ensures credit policies are well-defined, regularly reviewed, and enforced, while a risk-aware culture encourages disciplined decision-making across the organization. Together, they provide the foundation that maintains lending standards, even during periods of economic stress.

How to do it:

- Define clear credit policies that outline borrower eligibility, approval authorities, collateral requirements, and risk tolerances.

- Require regular review and approval of credit frameworks and portfolio performance by senior management and the board.

- Use independent credit review functions or risk committees to audit loan decisions and ensure compliance with policy.

- Provide ongoing training so staff understand both the “what” and the “why” behind credit standards and risk expectations.

- Align incentives and compensation with long-term portfolio performance, rather than short-term loan volume.

Benefits and challenges of credit risk management

To manage credit risk effectively, banks need a clear understanding of both the advantages of strong risk controls and the challenges that accompany them. Here are the pros and cons of credit risk management:

Benefits:

- Enhanced profitability: By identifying and managing high-risk exposures early, institutions can protect earnings, improve portfolio performance, and strengthen overall financial stability.

- Sustainable growth: Risk management enables banks to make informed lending decisions based on well-defined risk standards. By approving loans that align with their risk appetite, banks can responsibly grow their loan portfolios, maintain asset quality, and support long-term financial stability.

- Regulatory compliance: Strong credit risk frameworks help institutions meet capital adequacy requirements and adhere to regulatory standards. This reduces the risk of penalties, reputational damage, and regulatory intervention.

- Improved borrower relationships: Transparent, risk-based lending practices create clarity for borrowers. Fair pricing and responsible lending decisions build trust, strengthen client relationships, and enhance customer satisfaction.

- Reduced systemic risk: Institutions that maintain disciplined credit risk practices contribute to the overall stability of the financial system.

Challenges:

- Data availability and quality: Accurate credit decisions depend on comprehensive, up-to-date borrower information. Collecting, verifying, and maintaining high-quality data can be complex, especially when dealing with incomplete records or rapidly changing financial situations.

- Model accuracy and calibration: Credit scoring and risk models must continuously reflect evolving market conditions and borrower behavior. Poorly calibrated models can lead to inaccurate risk assessments, resulting in either increased credit losses or missed lending opportunities.

- Economic and regulatory uncertainty: Shifts in economic conditions, interest rates, or regulatory requirements can quickly impact credit portfolios. Institutions must remain agile and adaptable in order to successfully manage risks during periods of volatility.

- Technological disruption: Advancements in data analytics, artificial intelligence, and machine learning offer powerful tools for risk management. However, keeping pace with technological change requires ongoing investment, skilled talent, and system upgrades.

- Balancing analytics with human judgment: While quantitative models provide valuable insights, they cannot fully replace professional expertise. Effective credit risk management requires combining data-driven analysis with experienced judgment to account for qualitative factors and unique circumstances.

Strengthen credit risk management and fraud controls with VALID

Credit risk is no longer limited to borrower default alone. Fraud, operational breakdowns, and payment integrity failures increasingly drive unexpected losses, weaken portfolio performance, and distort credit decisioning.

To manage credit risk effectively, financial institutions need real-time, intelligence-driven risk controls that operate at the transaction level. This is exactly where VALID can help you.

VALID helps financial institutions reduce credit losses by addressing one of the fastest-growing contributors to portfolio risk—payment and deposit fraud that undermines credit quality, liquidity, and customer trust.

By combining real-time machine learning, behavioral analytics, and network intelligence, VALID enables banks to detect risk earlier, intervene faster, and protect both earnings and customer experience.

How VALID can help you:

- INclearing Loss Alerts: Uses advanced AI and behavioral analytics to identify abnormal patterns during transaction processing, uncovering risks that traditional detection systems often miss.

- CheckDetect: Proactively identifies suspicious activity across mobile, ATM, and in-branch transactions, enabling banks to prevent fraud in real time rather than responding after losses occur.

- Fraud Consortium Edge: A collaborative intelligence network built through partnerships with leading US banks, delivering broader fraud insights and early visibility into emerging threat patterns while upholding rigorous data privacy standards.

- InstantFUNDS©: Provides sub-second decisioning for check deposits, balancing fraud risk and customer experience by offering guaranteed funds availability when appropriate.

Contact us today to strengthen your credit risk management with real-time fraud intelligence that protects your portfolio, earnings, and customer trust.