As financial systems become increasingly complex and data-driven, traditional risk models often struggle to keep pace with rapidly evolving threats and uncertainties.

That is why many financial institutions are turning to machine learning that enables real-time analysis of vast datasets, leading to smarter credit decisions, stronger fraud detection, and more accurate regulatory compliance.

In this article, you will learn everything about machine learning in banking risk management so you can identify, assess, and mitigate risk more effectively.

Key takeaways

- Machine learning upgrades how banks manage risk

ML goes beyond static rules and traditional models. It learns from large datasets to detect complex patterns in credit, fraud, compliance, and operational risk. This results in more accurate decisions and fewer costly errors.

- Real-time, adaptive monitoring is now critical

ML enables continuous transaction monitoring and anomaly detection. Banks can spot suspicious activity instantly, even when fraud patterns are new. This helps institutions respond faster as threats evolve.

- Governance, fairness, and explainability are essential

ML models must be transparent and regularly tested for bias. Strong data governance, explainable AI tools, and human oversight are required to meet regulatory standards and maintain trust.

- Automation drives efficiency and scalability

ML automates routine, low-risk decisions. This reduces manual workload and speeds up approvals from days to seconds. Teams can focus on high-risk or complex cases.

- The right partner turns ML into measurable results

Successful implementation requires real-time decisioning, shared data insights, and built-in compliance controls. VALID delivers predictive, guaranteed fraud protection that reduces losses, lowers false positives, and strengthens overall risk management.

What is machine learning in banking risk management?

In banking risk management, machine learning (ML) refers to the use of data-driven algorithms to identify, measure, and manage different types of risk.

Traditionally, banks relied on statistical models (e.g., linear credit scoring) or static rule-based engines (e.g., flagging payments above a fixed threshold).

ML goes further by learning from the data itself. It can uncover subtle, non-linear relationships in customer behavior or market signals that old models miss.

Banks typically use different ML methods depending on the risk problem:

- Supervised learning is trained on historical, labeled data where outcomes such as defaults or fraud are already known. It is commonly used for credit risk modeling and fraud detection because it can predict the likelihood of known events.

- Unsupervised learning and anomaly detection focus on identifying unusual or out-of-pattern behavior without predefined labels. These methods are especially useful for spotting suspicious transactions, novel fraud schemes, or emerging risks that have not been seen before.

How does machine learning work in banking?

Machine learning in banking follows a structured process that transforms raw data into actionable risk decisions. Here is how it works:

Step 1: Collect and prepare data

Banks begin by gathering data from multiple sources, including internal records (such as transaction histories, loan data, and customer interactions) and external inputs (credit bureau scores, market indicators, news, and sanctions lists).

This data is then cleaned, standardized, and preprocessed to ensure accuracy and consistency before modeling.

Step 2: Engineer features and train models

Next, data scientists convert the prepared data into practical features, such as debt-to-income ratios, credit utilization, or spending patterns.

Machine learning models are trained on historical outcomes to learn the connections between these features and different risk types. For example, supervised models can learn to predict loan default based on past repayment behavior.

Step 3: Generate risk scores and alerts

Once trained, models are used to evaluate new cases. Credit models score loan applicants and estimate default risk or pricing recommendations.

In parallel, anomaly-detection models monitor transactions for fraud or compliance issues by learning normal behavior and flagging unusual activity, even when no predefined rule exists.

Step 4: Update, validate, and explain models

As new data becomes available, such as loan outcomes or confirmed fraud cases, models are retrained or refined. Banks regularly validate performance to ensure models remain accurate over time.

Also, explainability tools are applied to help risk managers understand why a model produced a particular result, supporting regulatory and governance requirements.

Step 5: Integrate into risk workflows

Finally, model outputs are embedded into operational decision-making. Low-risk cases may be approved automatically, while higher-risk or uncertain cases are routed to human reviewers.

With ongoing oversight and governance, these models become core components of modern banking risk management, enabling faster, more consistent decisions.

Benefits and challenges of using machine learning in banking risk management

Machine learning provides powerful tools for improving banking risk management by enabling faster, data-driven, and more adaptive decision-making.

However, these advantages come with important limitations and risks related to transparency, bias, and governance. Below are the key pros and cons you should consider.

Benefits:

- Improved accuracy: Machine learning uncovers subtle patterns in large datasets that traditional, rule-based models often miss, leading to more reliable predictions. In areas like credit scoring, this means fewer errors, safer lending decisions, and reduced fraud, while also lowering costs and improving the customer experience.

- Enhanced fraud and compliance detection: ML enables continuous, real-time monitoring, allowing banks to spot suspicious activity faster and with far fewer false alerts. As a result, institutions can detect more genuine fraud cases and enable human analysts to focus on the highest-risk situations.

- Operational efficiency: By automating routine decisions and data-heavy tasks, ML dramatically reduces processing time and operational costs. Lending decisions that once took days can happen in seconds, while onboarding, reporting, and document review become faster and more scalable.

- Dynamic adaptation: Unlike static rules, ML models learn and evolve as new data becomes available. This allows banks to quickly adjust to changing fraud tactics or economic conditions, such as shifts in interest rates or employment trends.

Challenges:

- Bias and fairness: Machine learning models can unintentionally reinforce historical biases embedded in their training data, leading to unfair outcomes in areas such as lending. Preventing discrimination requires ongoing bias testing, careful feature selection, and strong governance to ensure decisions remain fair and compliant with regulatory expectations.

- Transparency and explainability: Many advanced ML models operate as “black boxes,” making it difficult to explain how decisions are made. To maintain trust with customers and regulators, banks must invest in explainable AI tools, thorough documentation, and processes that make model decisions understandable.

- New fraud risks: Fraudsters are using AI too, creating more sophisticated scams such as deepfake identities and AI-generated documents. This creates an ongoing arms race, requiring banks to continuously strengthen and retrain their models to defend against emerging threats.

- Data and model risk: Effective ML depends on high-quality, representative data, which can be difficult to obtain, especially for rare events like fraud. In addition, model risk remains a major concern, requiring rigorous validation, oversight, and specialized talent that is often in short supply.

- Regulatory uncertainty: AI governance frameworks are still evolving, leaving banks to interpret how existing rules apply to new technologies. As standards continue to develop, institutions must stay agile and prepared for increased scrutiny or future AI-specific regulations.

How to implement machine learning in banking risk management

The following best practices outline how financial institutions can deploy ML in risk management while maintaining accuracy, regulatory compliance, transparency, and security.

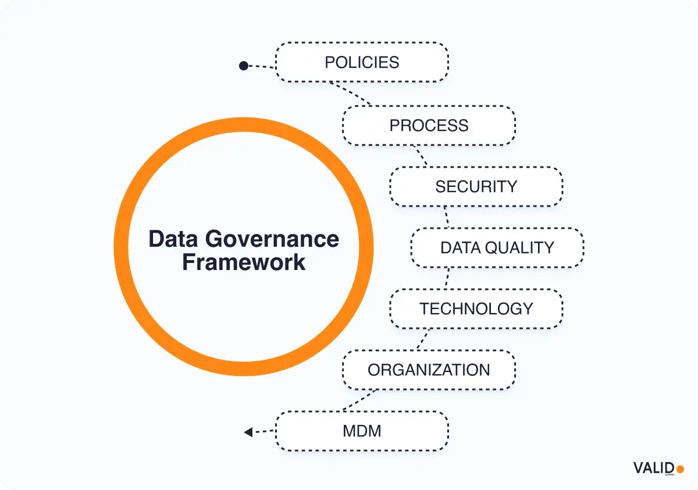

1. Strengthen data quality and governance

Machine learning models are only as good as the data they are trained on. In credit risk management, inaccurate, outdated, or biased data can lead to misleading risk scores and poor decisions.

To maintain model effectiveness over time, banks must also account for changing customer behavior and economic conditions, as these factors can degrade models if left unchecked.

How to do it:

- Establish robust data governance frameworks to ensure data is accurate, complete, and representative of the target population.

- Build automated data-cleaning and validation pipelines to detect missing values, inconsistencies, and anomalies before data enters models.

- Cross-validate key data elements using multiple sources where possible (for example, comparing information across different credit bureaus or internal systems).

- Regularly monitor for data drift and population shifts that signal changes in borrower behavior or market conditions.

2. Ensure regulatory compliance and fair lending integrity

Financial regulators such as the OCC, Federal Reserve, and NCUA expect AI-driven models to comply fully with existing banking and consumer-protection laws.

In lending, this primarily requires adherence to ECOA and HMDA, as well as compliance with formal model risk management and governance standards.

How to do it:

- Align AI credit models with ECOA (Regulation B), ensuring that applicants are not discriminated against based on protected characteristics (race, gender, age, etc.), either directly or through proxy variables.

- Use HMDA data monitoring to detect potential patterns of disparate impact in mortgage lending decisions.

- Apply model risk management standards consistent with supervisory guidance, such as the Federal Reserve’s SR 11-7 (model risk management), including independent validation, performance monitoring, and robust documentation.

- Conduct regular fair-lending and disparate-impact testing, including segmentation analysis across protected and control groups.

- Align practices with recognized industry frameworks such as the NIST AI Risk Management Framework and US Treasury AI guidance for the financial sector, both of which emphasize fairness, transparency, accountability, and bias mitigation.

- Incorporate explainability tools (e.g., feature importance analysis, adverse action reason codes) to meet ECOA’s requirement to provide clear explanations for credit denials.

3. Maintain explainability and human oversight

Advanced ML models can be complex and difficult to interpret, creating challenges for transparency and accountability in credit decision-making.

To manage this risk, institutions should ensure that AI systems support human judgment, with clear mechanisms for review, challenge, and override.

How to do it:

- Train credit and risk teams to understand model logic, limitations, and appropriate reliance boundaries.

- Define decision-tier thresholds that mandate human review for high-exposure decisions, low-confidence model scores, or applications involving thin-file or non-traditional borrowers.

- Require structured override governance with documented rationale, secondary approval for material exposures, and periodic analysis of override frequency, direction, and performance impact.

- Use explainability tools such as SHAP (Shapley Additive Explanations) to provide feature-level attribution for individual decisions.

- Maintain segregation of duties by prohibiting model developers from holding final credit approval authority.

4. Strengthen security and data privacy controls

AI and ML systems in banking operate on highly sensitive customer and financial data, making them attractive targets for data breaches, model theft, and adversarial manipulation.

Effective ML governance, therefore, requires integrating cybersecurity, data protection, and privacy controls directly into model development and deployment.

How to do it:

- Secure end-to-end ML data pipelines by controlling data ingestion, validation, storage, and access to reduce exposure to data poisoning and unauthorized manipulation.

- Limit the use of sensitive customer data by applying anonymization or data masking techniques whenever they do not materially affect model performance.

- Restrict access to ML data and models using role-based permissions so only authorized personnel can view, modify, or deploy them.

- Continuously monitor model inputs and outputs for unusual patterns that could signal adversarial activity or attempted manipulation.

- Integrate AI systems into existing cybersecurity and incident response processes to detect and handle potential AI-related breaches quickly.

- Maintain detailed logs and version histories for datasets and models to support audits, investigations, and regulatory reviews.

Use cases of machine learning in banking risk management

Here are some of the most well-known use cases of machine learning in banking risk management:

1. Upstart (credit union and bank lending)

Upstart is a US-based AI-driven lending platform used by hundreds of banks and credit unions. Instead of relying on traditional FICO credit scores, Upstart uses machine learning models that analyze 1,000+ variables to assess borrower risk more accurately.

These variables include:

- Income

- Education

- Job history

- Bank account activity

- Other non-traditional financial indicators

According to Upstart, compared to traditional FICO-only models, its platform delivers:

- 40–44% more loan approvals

- 36–43% lower interest rates for borrowers

- No increase in default rates

- 73% fewer losses at the same approval rate

- Approximately 80% of loan decisions fully automated

- Processing time reduced from days to seconds

2. Wells Fargo (fraud prevention and anti-money laundering)

Wells Fargo uses real-time ML models to monitor transactions and identify suspicious activity across fraud prevention, AML, and name-screening processes. Key elements of this approach include:

- Real-time transaction monitoring to detect fraud and potential money-laundering activity

- Transaction risk scoring based on unusual patterns, such as atypical transfer amounts, frequency, or timing

- Signal aggregation combining customer behavior history with external threat intelligence

- Advanced anomaly detection that identifies risks traditional rule-based systems may miss

3. American Express (card transactions)

American Express employs machine learning to detect fraud in real time across its global card network.

With more than 100 million cards in use worldwide, Amex relies on ML systems that continuously learn normal customer behavior and merchant activity. Core components of this approach include:

- Real-time transaction analysis across Amex’s 24/7 global payments network

- Behavioral modeling that learns individual customer spending patterns and merchant profiles

- Instant anomaly detection, flagging transactions that deviate from expectations (e.g., unusual merchants or locations)

According to American Express, its ML models identify approximately $2 billion in potential fraudulent transactions each year before losses occur.

Strengthen risk management with real-time fraud decisioning

As fraud tactics evolve, especially in check fraud, remote deposit capture (RDC), and cross-channel activity, financial institutions need more than traditional models to fight it.

They need real-time, predictive, and guaranteed decisioning tailored to today’s evolving fraud threats.

This is why VALID is trusted by leading institutions such as PNC Bank, TD Bank, and Truist.

VALID Systems is a financial technology company specializing in fraud prevention and risk management solutions for banks, financial institutions, and credit unions.

Leveraging advanced machine learning, behavioral analytics, and industry data collaboration, VALID enables organizations to reduce fraud losses, strengthen compliance, improve operational efficiency, and enhance the customer experience.

Why you should try VALID:

- Real-time fraud detection – Instantly identify and prevent check fraud across mobile, ATM, and in-branch deposits, enabling proactive loss prevention with minimal operational disruption.

- Reduced losses and false positives – VALID’s CheckDetect technology captures up to 95% of fraud losses while reducing false positives by up to 40%, allowing teams to prioritize high-risk alerts more effectively.

- Operational efficiency through automation – Decisioning based on machine learning streamlines fraud reviews, shortens investigation cycles, and reduces manual effort, enabling teams to focus on higher-value analysis.

- Smarter, data-driven risk decisions – Through the Edge Data Consortium, institutions access shared, anonymized industry fraud data to identify emerging threats earlier and improve forecasting accuracy.

- Comprehensive, multi-channel fraud coverage – From check fraud and account takeovers to loan application fraud, VALID delivers unified protection across multiple threat vectors through an integrated risk management approach.

- Guaranteed risk protection – VALID's guaranteed loss coverage model absorbs the cost of covered deposit losses, providing financial institutions with greater confidence and financial stability.

Contact us today to strengthen your fraud strategy with real-time, predictive, and guaranteed decisioning, and stop evolving threats before losses occur.